Economic Divide Between Boomers and Younger Generations

Younger generations — particularly Millennials (1981–1996) and Gen Z (1997–2012) — face structurally tougher economic conditions than Baby Boomers did at the same age. The common Boomer-era argument that younger people are simply “lazy,” “frivolous,” or should “just get two jobs” oversimplifies a far more complex economic reality. Current data shows significant headwinds in housing affordability, education costs, wage growth, and wealth accumulation.

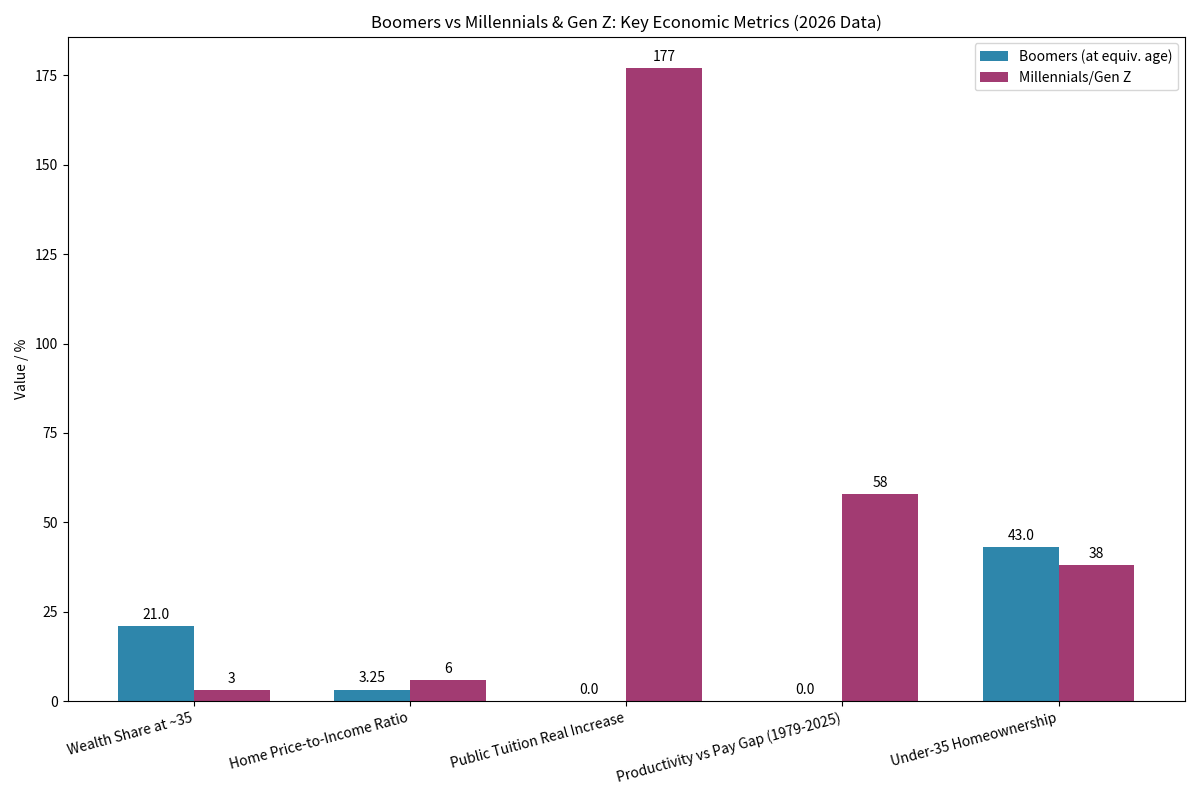

Wealth Gap

Baby Boomers currently hold roughly 51% of U.S. household wealth, totaling approximately $85 trillion. Millennials and Gen Z together control only around 10–11%. At roughly age 35, Boomers held about 21% of national wealth in 1989, whereas younger generations today hold closer to 3% at a similar life stage. Median net worth among younger cohorts significantly lags behind previous generations when adjusted for age and timing.

Income and Productivity

Between 1979 and 2025, worker productivity increased by approximately 92%, while typical worker compensation grew only about 34%. Younger workers produce substantially more economic output than previous generations but capture a smaller share of the gains. Economists commonly attribute this gap to globalization, declining union participation, automation, and broader policy changes that shifted bargaining power away from labor.

Housing Costs

Housing represents one of the clearest generational disadvantages. Median home prices are now more than 107% higher in real terms than they were during the 1980s. Price-to-income ratios have risen from roughly 3–3.5× annual income to 5–7× or higher in many markets. Homeownership among Americans under 35 sits around 38%, notably below the trajectory experienced by Boomers at the same stage of life. Rental costs have also climbed sharply, placing heavier financial burdens on younger households.

Education and Debt

The cost of higher education has risen dramatically. Public college tuition has increased approximately 177% in real terms over the past several decades. Millennials carry an average student debt burden of around $33,000, while Gen Z borrowers average roughly $22,000. These obligations delay homeownership, investing, marriage, and long-term wealth building.

Labor Market Reality

Despite stereotypes, younger Americans are not participating less in the workforce. Prime-age labor force participation remains near record highs at roughly 84%. Job tenure among 25–34-year-olds averages about 2.7 years, nearly identical to Boomers at the same age. Multiple-job holding rates are not dramatically higher than in prior decades, and rising costs for childcare, transportation, and healthcare often make maintaining multiple jobs less practical than many older Americans assume.

Spending Habits

Younger generations do spend more on technology and experiences than previous generations did. However, essentials such as housing and healthcare now consume more than 46% of household budgets, compared to roughly 25% during the youth of many Boomers. Claims that “frivolous spending” explains generational struggles overlook the reality that discretionary purchases represent only a small fraction of the broader affordability gap.

Conclusion

Structural economic factors — including asset inflation, wage stagnation relative to productivity, and rapidly rising costs in housing, education, and healthcare — explain much of the generational divide. Younger Americans generally work comparable hours to prior generations but face significantly worse affordability conditions. While some advantages exist today, such as cheaper consumer goods and the prospect of future inheritance transfers, the broader economic data demonstrates that Millennials and Gen Z are navigating a genuine financial squeeze rather than merely displaying weaker work ethic or poorer financial discipline.